Two decades ago, the thinking was that diagnostics would be largely conducted at the molecular level. It was anticipated that technologies capable of identifying a pathogen or a gene with high sensitivity just might displace tests based on associated antibodies or certain proteins. That hasn’t happened. Traditional chemistry and ELISA testing still account for a major part of the laboratory workload.

Yet, there has been progress. Molecular-based diagnostics now accounts for one-eighth of the total market. Moreover, the opportunity for growth and the greatest promise for improved outcomes in so many diseases is in the molecular area.

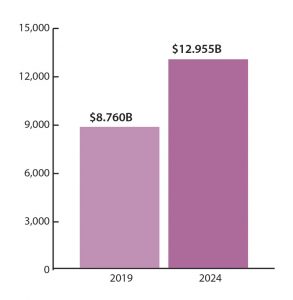

The market for molecular diagnostics is worth some $8.760 billion and expected to grow to $12.955 billion in 2024 (Figure 1). This means that molecular tests are experiencing revenue growth that is nearly triple the average for traditional in vitro diagnostics (IVDs), according to the eighth edition of Kalorama’s World Market for Molecular Diagnostics, which was released in June.1 (New editions appear every two years.)

What’s fueling this growth? A desire for better outcomes and accuracy, as well as more detailed identification of antigens, tumors, and mutations, helps explain the success. But the market is also getting a boost from advances in molecular technologies, including a migration from traditional methods and also improvements to features of those methods, which have the effect of boosting prices and thus the market.

A shifting technological lineup

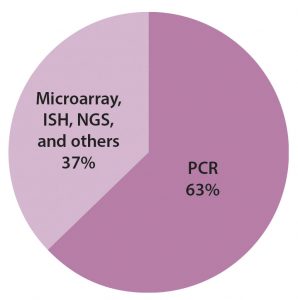

The bulk of that revenue comes from the same technology that originated it: polymerase chain reaction (PCR) technology. PCR-based testing still represents a high-growth segment. As indicated in Figure 2, it accounts for more than half of the molecular-based testing market. Other segments in this market correspond to different technologies, such as isothermal nucleic acid amplification technology (INAAT), in situ hybridization (ISH), microarrays, and next-generation sequencing (NGS).

An evolution is happening within the scope of molecular testing. Hybridization-based testing technologies such as microarrays and ISH are being superseded in clinical practice by quantitative PCR (qPCR) technology and NGS. The latter category is the most interesting.

NGS is making a rapid run. Illumina, Thermo Fisher Scientific, and other vendors are reporting improved clinical sales, and more systems are being used in diagnostic decisions.

The first NGS system was approved for clinical use by the FDA in 2013, so the market segment is quite new. However, a significant industry already exists for laboratory developed tests (LDTs) performed as testing services on NGS platforms by certified clinical labs. NGS is increasingly used for clinically heterogeneous inherited disorders, resulting in an increase in the number of reported disease-causing genes.

Currently, the NGS technologies mainly used in clinical laboratories are the Ion Torrent and Illumina systems. The Ion Personal Genome Machine (PGM) was launched in 2011 by Life Technologies (now part of Thermo Fisher). The more popular Illumina benchtop systems for diagnostic purposes are MiSeq (launched in 2011), MiniSeq (launched in 2016), and iSeq 100 (launched in 2017).

Nucleic acid microarrays are also used in diagnostics. These chip surfaces feature dozens to thousands of microscopic spots, each populated by probes specific to one target sequence within a sample. Genotyping is the main clinical application of microarrays today in various application segments covering noninvasive prenatal tests, postnatal testing, tissue typing, and infectious disease tests, as well as patient genotyping related to pharmacogenomics or rare diseases.

Microarrays are cost-effective, but they have lost market share in many applications. Immucor’s high-complexity molecular immunohematology kits are among the few FDA-approved microarray test kits introduced in recent years.

ISH refers to the direct probing without enzymatic amplification of nucleic acid targets within sample cells or tissue. The method typically utilizes a nucleic acid probe sequence attached to a reporter molecule to quantify and localize a target nucleic acid sequence (DNA or RNA) within a cell or tissue sample.

Protocols require a lot of hands-on time, and it usually takes at least half a day to obtain results. Experienced personnel and professional interpretation of the results are required, often aided by automated image analysis software. The trend now is to produce fully automated ISH systems to reduce the time and personnel required, improving cost-efficiency. Companies offering these automated services include Accelerate Diagnostics, Leica Biosystems in partnership with Advanced Cell Diagnostics (ACD), and INTAVIS Bioanalytical Instruments.

A need to establish clinical utility

The potential of molecular diagnotics technology, like that of any diagnostics technology, depends on clinical utility. Coverage by Medicare and other payers for a molecular diagnostics product or test can be obtained through the demonstration of its clinical utility, particularly in terms of how a test can improve patient outcome.

Proving the utility of a test involves clinical data generation. It is also necessary to evaluate analytical validity (or the accuracy, precision, and reproducibility of test results) and clinical validity (or how well a test can determine the presence, absence, or risk of disease). Definitive clinical utility is becoming a criterion for the market success of new molecular diagnostics, particularly in the case of high-priced, advanced tests without comparable products on the market.

Clinical utility may also be defined more broadly. This point was emphasized by a report issued by the Association for Molecular Pathology (AMP) in 2016. According to the AMP, therapy-aligned definitions of clinical utility are too narrow because they fail to capture the value that tests can provide through additional prognostic criteria and predictive capabilities, including those relevant to patients’ family members.

However, the expanded scope for clinical utility proposed by AMP is incompatible with U.S. health insurance outside of family plans, where testing of one parent may inform medical care of children also potentially at risk. Payers otherwise have no incentive to pursue testing unrelated to patient outcome since improved outcomes for family outside of children on the same plan would deliver no value to payers.

Developed and emerging markets

As in most IVD markets, sales to emerging markets are a way to counter some of the resistance and payment schemes in developed markets. China is one of the fastest-growing molecular diagnostics markets. It has a population of over 1.4 billion, which is growing at 0.5% per year.

China’s growing urban middle class is demanding more services, spurring the development of private laboratories. The number of new independent clinical laboratories (ICLs) has grown substantially from 2016 to 2017, with more individual labs focusing on advanced methods such as gene sequencing technologies.

Increased spending in China and the progress of NGS product launches, test approvals, and sales will be key in assessing the future growth for this important testing market.

Bruce Carlson ([email protected]) is the publisher of Kalorama Information, part of Science and Medicine Group.

Reference

1. kaloramainformation.com/product/the-world-molecular-diagnostics-market-8th-edition