August 1, 2009 (Vol. 29, No. 14)

Widespread Screening Practices for All Patients Responsible for Growth in HPV and MRSA Testing

Molecular diagnostic tests for infectious diseases are proving to be one of the highest-growing segments of the in vitro diagnostics market. Accordingly, companies that participate in the clinical diagnostics industry understand that their market participation might be crucial to their future success. However, some segments of the infectious disease molecular diagnostics market are already well established and don’t offer much of an addressable opportunity for new market entrants. Therefore, it’s vital that companies understand where the true opportunities remain.

The technology is complex and labor-intensive, limited only to clinical laboratories with the resources and skilled staff that can meet CLIA requirements. Furthermore, the tests are expensive and run on different systems that end-users would have to install should they wish to perform them.

The molecular diagnostics market is fragmented, and there is no single vendor that can provide a comprehensive suite of products. Thus, only clinical laboratories with substantial resources for implementation can position themselves to provide molecular diagnostics to the medical community.

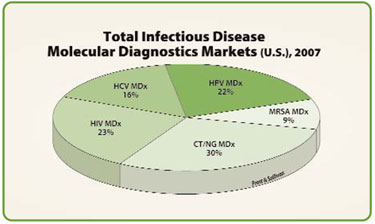

Given the small test menu on each system, it is primarily the size of the test volume that warrants adoption. Large national laboratories have the economies of scale to provide molecular diagnostics. Naturally, the largest segments in the molecular diagnostics market are human immunodeficiency virus (HIV) testing, hepatitis C virus (HCV) testing, and Chlamydia trachomatis (CT) and Neisseria gonorrhea (NG) testing.

The growth rates in these market segments have been stagnant, even declining. The markets are saturated, and the competition is intense. Two emerging molecular diagnostics markets, however, are enjoying rapid growth rates and even have the potential to surpass the market size of the more established infectious disease tests. The two emerging molecular diagnostics markets are human papillomavirus (HPV) testing and methicillin-resistant Staphylococcus aureus (MRSA) screening.

Total infectious disease molecular diagnostics markets (U.S.), 2007

HPV Diagnostic Market

HPV, a sexually transmitted virus, has been clinically proven to be the primary cause of cervical cancer. This virus has been found in more than 99% of cervical cancers, and it continues to be one of the most astounding medical findings that an infectious disease can cause cancer.

In the U.S. and other developed countries, widespread screening programs have been in place for decades to reduce the incidence of cervical cancer. The introduction of the Pap test more than 50 years ago transformed the management of cervical cancer.

The Pap test, however, is subjective in nature and found to have a clinical sensitivity of roughly 80%. The stains used to identify deformed cells as a result of persistent HPV infection can be difficult to interpret. Direct testing for HPV with molecular diagnostics is entirely objective and when combined with the Pap test, clinical sensitivity is virtually 100%. There is tremendous value in HPV testing in the fight against cervical cancer and test volumes continue to soar.

MRSA Diagnostics Market

The abuse of antibiotics has led to the rise of multidrug-resistant organisms (MDROs). MRSA is the most prevalent of such MDROs with vancomycin-resistant enterococci following behind. These mutated strains are of increasing concern and pose serious public health issues.

With fewer effective antibiotics available, infections caused by MDROs are becoming harder to treat and are associated with significantly higher rates of mortality and morbidity, longer hospital stays, and, consequently, greater healthcare costs. It is estimated that there were approximately 370,000 hospital stays for MRSA infections in 2005 in the U.S., and these stays cost an average of $14,000 versus $7,600 for all other stays. This equates to $2.4 billion in excess healthcare costs. This figure is likely to increase as MRSA screening programs continue to uncover higher infection rates.

Infectious Disease

The molecular diagnostics market for CT/NG, HIV, and HCV testing are centered on diagnosis and disease monitoring, but the emerging HPV molecular diagnostics market and the MRSA molecular diagnostics market are based on widespread screening practices for all potential patients. The test volume is thus larger and industry participants will be able to capitalize on plenty of lucrative opportunities.

In 2007, the HPV molecular diagnostics market and the MRSA molecular diagnostics market generated $192.8 million and $80.7 million in revenues, respectively, in the U.S. In comparison, the combined market for CT/NG molecular diagnostics, HIV molecular diagnostics, and HCV molecular diagnostics totaled an estimated $600 million. The HPV and MRSA molecular diagnostics markets have the potential to grow to more than $2 billion.

Kevin Leong ([email protected]) is a consultant in the clinical diagnostics group of Frost & Sullivan. Web: www.frost.com.