October 1, 2009 (Vol. 29, No. 17)

End-User Resistance, Legislative Hurdles, and Limited Competition Have Skewed Predictions

Even if legislative hurdles are worked out, the U.S. market for biosimilars may not be the multibillion dollar market that many analysts have projected. But that doesn’t mean there won’t be robust competition. Long-term, generic competition will still change the way biopharmaceuticals are sold in the United States.

The $40 billion biopharmaceutical market including vaccines, most new cancer agents, and arthritis and psoriasis drugs is the fastest growing segment of the pharmaceutical industry. Some of the most expensive drugs in the world are biologics.

Biopharmaceuticals account for about 250 of the more than 10,000 drugs on the market, but represent a disproportionate share of the nation’s healthcare spending, costing Medicare Part B more than $12 billion in 2008. Since the generic industry has done much to reduce pharmaceutical costs in the past 25 years, it’s no wonder that many are looking to generic competition to reduce the costs of biologics.

The term biosimilars is used since, unlike generic pharmaceuticals, there are no truly exact biologic replica due to the complex process of creating biopharmaceuticals, so generic products are either similar in nature or in some cases improvements over the original. There currently is no pathway for these products in the U.S. market, but recent House and Senate committee approvals portend some kind of mechanism for U.S. approvals by next year.

At the time of writing, Congress is still deciding whether the exclusivity period for biological products will be set at 5 or 12 years. Biosimilars likely to enter the U.S. are first-generation products such as human growth hormone (HGH) and insulin, as well as second-generation products such as protein and recombinant DNA treatments.

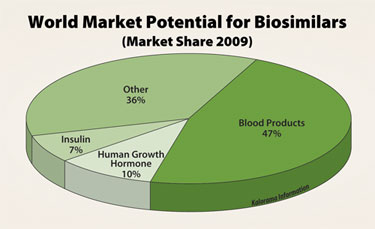

World market potential for biosimilars (market share 2009)

Market Size

As of 2008, Kalorama Information estimates a $60 million biosimilar market in the European Union. A variety of factors have contributed to this diminished market size, including end-user resistance. Also, rather than the scores of entrants in this marketplace that were expected, competition is limited and typically against branded drugs rather than other generic drugs. The production and distribution competency required for the biosimilar process severely limits the number of players.

The robust competition among a few experienced and strongly funded competitors will create a U.S. market for biosimilar drugs that Kalorama Information estimates could reach $30 million by 2013. As products develop, the U.S. market will build over the next decade. We expect the same pattern that occurred in the generic industry in the ’80s. Slower than anticipated growth with some resistance at first, then a flourishing market. Our U.S. market figure may surprise some due to the generous predictions made when biogeneric approval was first discussed.

Don’t tell a product manager at an established branded biologic that U.S. biosimilars won’t be a significant headache. The total market may be smaller than previously projected, but those products that face biosimilar competition will need to change their business plans dramatically.

This does not mean there won’t be competitive activity, just that the field of play will be narrower than previously thought. Competition will open up between producers of biosimilars and producers of branded biopharmaceuticals if, as looks likely, Congress approves these drugs in the U.S.

It’s a small but experienced group that will lead the competition in the U.S. Some of the leaders emerging in the market are Cangene, Biocon, Sandoz, TEVA, and Dr. Reddy’s. Having successfully marketed biogeneric products in Europe and Asia, these companies will come prepared to the new market. Among biological products being challenged is Amgen’s chemotherapy drug Neupogen, which stimulates production of white blood cells, and Genentech’s Rituxan, a protein used in the treatment of rheumatoid arthritis and non-Hodgkin’s lymphoma.

Currently, the world market for biosimilars is fueled primarily by the demand for bioequivalent versions of erythropoietin and G-CSF. Sales for these products were estimated at $62 million in 2008. This includes sales for products in Europe and throughout the world where lenient biosimilar laws exist.

Insulin is a long-time favorite for biosimilar production with a relatively simple manufacturing method to follow. However, sales continue to be minimal in contrast to the total insulin market.

Another focus for biosimilar production in the United States and key markets in Europe is HGH. Sales, however, have failed to show the significant gains that manufacturers expected. Sales for bioequivalent HGH have been estimated at $15 million globally for 2008.

Long-Term Challenges

One of the biggest issues facing biogeneric products is the question of how to show bioequivalence. It is imperative to be able to show that two active ingredients are identical, this is difficult because biotechnology products tend to be complex in structure, heterogeneous, and produced by fermentation of living organisms. In addition, they typically have poorly understood structure, function, and clinical efficacy.

Another challenge that has emerged is whether there is sufficient availability of bulk material and bulk biogeneric suppliers. Several reliable contract biopharmaceutical producers are emerging; however, their focus has been mainly on exclusive custom manufacturing of new biologicals under development by biotech companies or pharmaceutical industry participants.

The question is, what strategies will contract biopharmaceutical producers adopt with respect to biogenerics? Will they eventually move into this market, risking alienating their present customer base, or will they instead stick to the innovator biopharmaceutical market? And will the industry be able to keep up with the demand?

Given the current capacity shortage for mammalian cell culture, it is quite likely that most contract biopharmaceutical companies will stick with present biopharmaceutical companies, making it difficult for biogeneric companies to gain access to bulk materials for their products.

Partnership among generic companies may help to solve the bulk material problem. There has been significant consolidation within the generic industry in the past few years, which should better position the industry to produce and compete within the biopharmaceutical market. Such competitive developments indicate a promising future for biosimilars. It may take a decade or more, but it is clear that there will be a strong generic biologic market in the U.S.

Bruce Carlson ([email protected]) is publisher at Kalorama Information. The company’s new report “World Market for Biosimilars and the Potential for U.S. Follow-on Biologics” can be found at www.kaloramainformation.com.