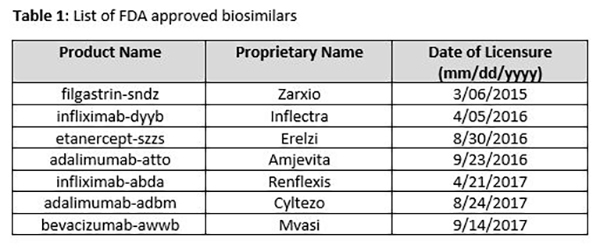

The biosimilars market is growing rapidly. The global market, currently valued at around $5 billion, is expected to exceed $28 billion by 2020. Over the past two years, seven biosimilars (Table 1) have been approved by the FDA, including two each for the anti-inflammatory drugs adalimumab and infliximab, and one each for filgastrin, etanercept and bevacizumab.

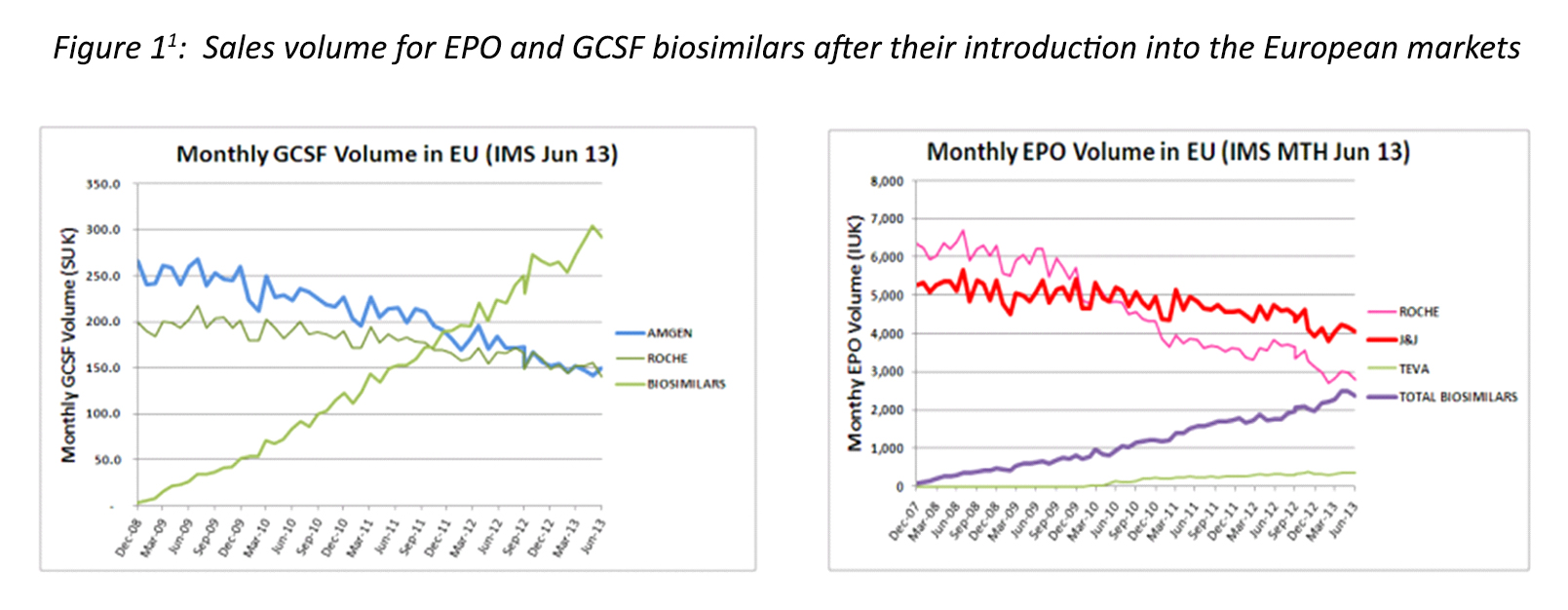

If Europe is a guide (Figure 1), the sales of biosimilars will continue to grow in the US, as physicians increase their rate of prescription, and patients become more comfortable using biosimilars.

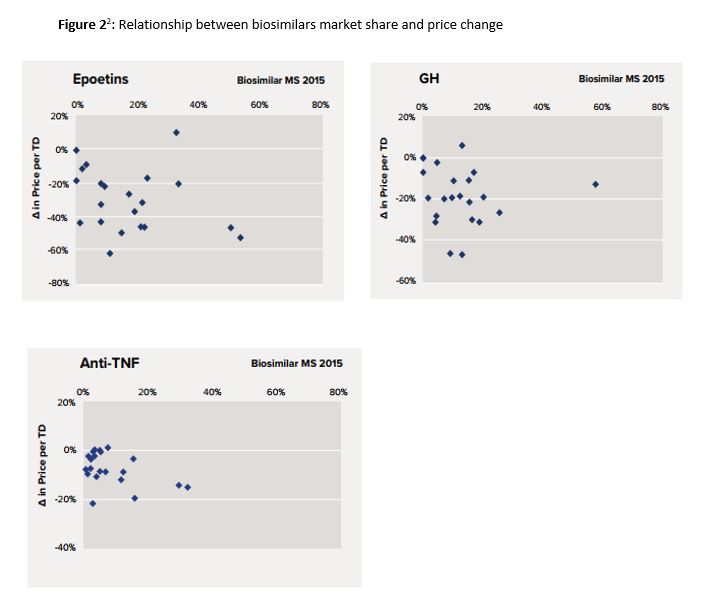

Furthermore, the introduction of more biosimilars to each type of biologics is expected to increase competition and drive down prices. Again, this phenomenon has been closely monitored in Europe (Figure 2) where a definite relationship has been observed between overall increase in biosimilar market share and price drop, albeit with relatively poor correlation, especially for growth hormone (GH).

In fact, the range of healthcare savings in the US from biosimilars is projected to range from $24 billion up to $150 billion between 2018 and 20273.

It is expected that biosimilar developers will further expand their reach by developing biosimilars to even newer innovators’ products such as Eylea, Lucentis, Stelara, Actemra, etc., thus continuing to expand competition and price pressure across these other product franchises. In addition, big selling vaccines, like the pneumococcal protein conjugate vaccines and the human papillomavirus (HPV) vaccines, will also be desirable targets for biosimilar development.

This increase in competition, along with decreasing prices for biopharmaceuticals, will benefit the consumers by increasing affordability and accessibility of these products to a larger proportion of the population. Still, while there are clear and measurable benefits to the consumer, the response among the developers of the innovator products has been somewhat inharmonious to the challenges presented by the emergence of biosimilars.

Several developers of originator products have pursued litigation, trying to stop biosimilars from entering the market place and there is no evidence this trend is waning. However, while this strategy might be somewhat effective in the short term, it is clearly not effective in the long run. Alternatively, some companies, expecting sizable reductions in revenues and profits, have been shrinking operations and laying off employees. Other innovative product companies have adopted more growth-driven strategies in response to biosimilars, including:

• Exploration of new clinical indications for their biopharmaceutical products

• Expansion into new markets

• Development of next generation biopharmaceuticals through:

º Internal R&D

º Acquisition of Intellectual Property

º Acquisition of start-ups and mid-size biotechnology companies with promising new

products/technologies

º Collaboration with other companies

• Development of their own biosimilar franchises

While the biopharmaceutical innovators strive to maintain their market shares in this new environment and protect their market share by introducing novel products, there is a strong push by biosimilar developers to innovate and increase efficiency through improvements in process development, manufacturing and testing. There are substantial improvements and efficiency gains in biosimilar manufacturing through the adoption of new strategies, including:

º Multi-product facilities

º Clinical/commercial scale single-use systems

º Continuous processing

º Improved expression systems, along with other genetic engineering advances

º Automation, monitoring, and improved process control

º Modular facilities that can be repurposed on demand

From the testing side, the availability of new analytical tools, especially high-resolution mass spectrometry (HR-MS), are benefitting biosimilar developers with faster product characterization and comparability assessment, as well as by streamlining product release and stability analysis. Improved production and analysis efficiencies ultimately translate into reduced product cost.

Thus far, biosimilar production has been primarily focused in Europe, and more recently the US. However, emerging countries with fast-growing economies, like China, India and certain regions of South America and Africa, represent large potential markets for biosimilars. There will be a large push by the bigger biosimilar developers to capture some of these markets. But, it should be noted that a substantial share of these markets will be most likely served by local biopharmaceutical companies, consequently propelling growth of the local biopharmaceutical sectors.

The emergence of biosimilars has shown to have had a sizable impact in lowering biopharmaceutical costs in Europe, and it is anticipated that such savings will be realized both in the U.S. and elsewhere globally. This reduction in costs will increase overall product affordability and availability, while also providing a surge in competition in biosimilar development. Ultimately, this will drive more innovation leading to the discovery of more novel technologies and therapies, as well as increased efficiency in both biopharmaceutical production and testing.

Mario DiPaola, Ph.D., is senior scientific director for Charles River Laboratories.

1. IMS Midas 2013

2. IMS Health 2016

3. RAND, 2017