Over the past five years interest in new and alternative downstream technologies has increased rapidly. This is due, in part, to the well-documented bottlenecks being created by improved upstream efficiencies. Incremental improvements are high on the list, such as evaluation of higher capacity resins, which are now being considered by over half the industry’s decision-makers. But the fastest growth in interest among biomanufacturers has been for prepacked disposable chromatography columns. Back in 2010, our Annual Report and Survey of Biopharmaceutical Manufacturing found that just 1% of the industry was interested in prepacked column technology. Over the past few years that interest has grown to over 27% of decision makers who said they were considering adopting these new technologies.1 That jump has pushed the technology to near the level of interest given to other technologies that have been in the market for longer, such as buffer dilution systems/skids and continuous purification systems.

Why the Interest in Prepacked Columns

“Disposable” columns are reported to often be used multiple times, due to the current cost of resins being packed, so few if any prepacked columns marketed today may be considered “single-use”. However, as the price of resins decrease, it is likely that these prepacked columns will move into the single-use category, as well. Prepacked columns are quick to set up, and offer operational flexibility with rapid changeovers. They simplify validation and cleaning, and allow for more runs, with reduced labor for activities like column testing, validation, and documentation. Other benefits include elimination (outsourcing) of noncore activities, and the benefits of receiving expert-packed, fully validated and documented columns, with smaller facilities potentially lacking needed specialized expertise and equipment.

External factors are also influencing growth, including the number of mAbs in development and clinical trials, biosimilar developments, and facility expansions using single-use strategies. Speed to market and change-over to next-candidate products are key decision factors. In the future, complementary technologies such as continuous processing methods will also impact future growth for prepacked disposable columns, as the need for consistency and efficiency moves the packing off-site.

Market Size for Disposable Downstream Technologies

Five years ago, there was substantial interest in alternatives to protein-A chromatography; according to our 10th Annual Report and Survey of Biomanufacturing1, 60% of the industry was evaluating these options for new production. Today, that number has dropped by nearly half, to just 33% of biomanufacturers. However, other options continue to grow in interest due to the continued pressure on downstream purification technologies to keep up with improvements in manufacturing and yield. As a result, the potential market for these new technologies, especially those with disposable applications in larger-scale manufacturing, are likely to be substantial.

For example, the current size of the market for prepacked disposable columns used in bioprocessing (typically greater than 1 liter size), is around $45–$55 million. This estimate includes resins, materials, and services associated with prepacked columns. We note that some manufacturers pack columns using their own resins, while others provide packing services-only, using customer-provided or specified materials. This makes direct competitor comparisons difficult, especially given the high cost of some resins.

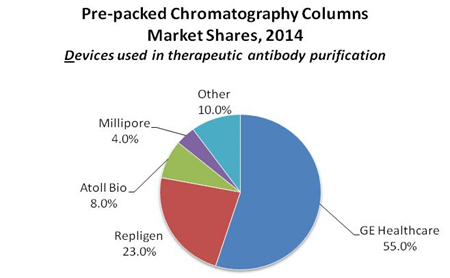

Prepacked column suppliers that pack using their own resins include GE Healthcare and EMD Millipore. Other suppliers prepack using various manufacturers’ resins as a service including Atoll Bio, Repligen, and other smaller service companies. As noted, in some cases, suppliers use their clients’ resins, and the high cost of these resins may not be included in market estimates.

The market for prepacked disposable columns is currently dominated by GE Healthcare, which launched its Ready-to-Process® columns 4–5 years ago. This has given GE a leading position spanning development- to commercial-scale. GE’s share of the chromatography resins market is substantial, and contributes to their dominance of the prepacked market, with around 55%. This share may be greater if resin revenues at retail levels are included (for example, GE’s largest Protein A columns may cost in excess of a quarter million dollars). Other companies, such as Repligen (>20% market share), Atoll Bio (~8% market share), Thermo Fisher/Life Tech, and EMD Millipore, Biotoolomics, Bio-Rad, Qiagen, and others, each with less than 10% market share.

The market is currently restricted by technological limitations of column size. Once larger, lower-cost single-use (or disposable) prepacked columns are made available for large-scale clinical and commercial applications, this market is likely to increase rapidly.

The market for prepacked columns is expected to see 10–15% growth in 2014, and up to 20% by 2016. These estimates are based on a market that is currently limited to clinical trial materials, because prepacked columns beyond the 30 cm diameter size are generally unavailable. As larger-scale columns (e.g., 45 cm–60 cm in diameter +) are developed and become commercially feasible, the market potential could expand significantly. Larger prepacked columns need to be developed that provide technical, economic, and logistical advantages.

Applications and New Technologies

A key early market for prepacked disposable columns is contract manufacturing organizations (CMOs) involved with multi-product facilities that offer clinical materials. In addition to CMOs, prepacked columns are also attractive to end-user companies building clinical trials facilities. For the time being, most prepacked columns are not at the size where they can be widely adopted by larger, commercial-scale manufacturing (typically beyond 30 cm ID). There are many applications for prepacked disposable columns, and they each present different market opportunities. Buyers include process development facilities, where prepacked columns allow convenience to evaluate many resins and formats, and pilot facilities, with fewer resources and time pressures that require different batches at difference sizes. For these facilities, packing of columns to follow GMP regulations is laborious and potentially risky.

The use of prepacked columns in pilot and clinical/commercial-scale GMP manufacturing is likely to become more competitive. The big question for large-scale commercial market penetration remains pricing, with the market likely not being persuaded to switch from in-house column packing without a significant cost motivation.

The prepacked column segment is also leveraging suppliers’ innovative expertise in resins, and services as well as designs that meet users’ needs. Just a few examples: EMD Millipore’s recently launched Chromabolt™ columns featuring ion exchange resins. Expect Protein A and other affinity resins in the next year or two. Atoll recently launched MaxiChrom AC™, Process-Scale Columns (single or campaign-use). Repligen launched its OPUS™ prepacked disposable columns, and is launching a 45 cm ID prepacked column in early 2014. And Thermo Fisher/Life Technologies recently offered its GoPure™ column.

Summary

The need for better single-use and disposable systems in downstream processing is growing. Our Annual Biomanufacturing Study has consistently indicated that incremental improvements in downstream chromatography steps are not resolving existing problems. Aspects such as the cost of Protein A resins, problems with packing columns, and the lack of cost-effective and large-scale disposable chromatography media and methods suggest that single-use technologies could alleviate many downstream issues. But so far few cost-effective alternatives exist. The move toward disposable upstream bioprocessing will push downstream operations toward innovative alternatives that may include membrane adsorbers and prepacked single-use chromatography columns.

Eric S. Langer ([email protected]) is president and managing partner at BioPlan Associates.

References:

110th Annual Report and Survey of Biopharmaceutical Manufacturing Capacity and Production, April 2013, Rockville, MD: www.bioplanassociates.com/10th

Survey Methodology: The 2013 Tenth Annual Report and Survey of Biopharmaceutical Manufacturing Capacity and Production yields a composite view and trend analysis from 238 responsible individuals at biopharmaceutical manufacturers and contract manufacturing organizations (CMOs) in 30 countries. The methodology also included over 158 direct suppliers of materials, services and equipment to this industry. This year’s study covers such issues as: new product needs, facility budget changes, current capacity, future capacity constraints, expansions, use of disposables, trends and budgets in disposables, trends in downstream purification, quality management and control, hiring issues, and employment. The quantitative trend analysis provides details and comparisons of production by biotherapeutic developers and CMOs. It also evaluates trends over time, and assesses differences in the world’s major markets in the U.S. and Europe.