By Missag Hagop Parseghian, PhD

Chief Scientific Officer and Co-Owner, Rubicon Biotechnology

Heart disease is the number one cause of death in developed nations and in many developing nations. Back in 2011, the American Heart Association projected that 40% of Americans would suffer from cardiovascular disease (CVD) by 2030. We hit that milestone in 2015. With 24 million deaths/year worldwide estimated by 2030 to be caused by CVD and stroke,1 you would think that there are major private financial investments being made for cardiac disease therapeutics. You would be sadly mistaken. Venture investment into oncology-focused drug development companies is 13 times greater than funding for CVD-focused enterprises, according to the Biotechnology Innovation Organization (BIO).2

This has serious consequences for those of us developing the next generation of medicines. Having spent 15 years working on cancer biologics prior to working on CVD therapeutics and co-founding Rubicon Biotechnology, the difference that I’ve observed in attitude among investors is surprising.

Last year, David Thomas, vice president of industry research at BIO, said the small size of the clinical pipeline for CVD indications was “very concerning.” He noted that in hypertension, there are only 6 drug programs for new chemical entities going after novel targets, and that in heart failure, there are only 17. By comparison, oncology has 2,600 novel chemical entities, most addressing novel targets. There are 150 drug programs going after novel targets for lung and breast cancer alone.

Why is this happening? CVD therapeutics are not so different from novel drugs for any other diseases, with attrition rates about the same at each phase of development. Less than 10% of drugs that begin clinical trials end up with an FDA approval. However, in the case of CVD therapeutics, there is the psychology of time.

Potential investors often cite the time it takes to enroll thousands of patients in clinical trials to obtain statistically significant data for FDA review. For investors, time is money. Cancer drugs generally require fewer patients and shorter follow-ups. An analysis of 448 pivotal clinical trials that led to FDA approvals between 2005 and 2012 found most cancer therapeutics required a single trial lasting 9–29 weeks and involving 84–610 patients. CVD drugs required at least three trials, each lasting 10–26 weeks and involving 406–926 patients.3 The differences are deceptively small until you consider the actual clinical trial history for a typical CVD biologic. (see Appreciating the Size and Length of Clinical Trials for CVD Therapeutics)

Then there is the psychology of fear. More Americans fear cancer than CVD (41% vs. 8%).4 Those perceptions hinder emerging companies like Rubicon Biotechnology interested in exploring the vast untapped potential of molecular biology to revolutionize cardiovascular healthcare. Over the past 20 years, only one new class of drugs has been approved for hypertension and only two new classes have been approved for heart failure.2

Learning from incentives for orphan drugs

We need to improve incentives that can “push” industry (for example, through reduced R&D costs) and “pull” industry (for example, through improved return on investment) into innovative CVD therapeutics. To enhance both push and pull, I argue that orphan drug incentives—the incentives that are used to encourage drug development for the rarest diseases—should be used to encourage drug development for the most common diseases.

Since 1983, the FDA has incentivized investment into rare diseases (that is, diseases affecting fewer than 200,000 patients in the United States) by providing potential therapies an orphan drug designation. Receiving the designation has both push incentives, such as tax credits, and pull incentives, such as a seven-year period of exclusive marketing after drug approval.

Since 2000, the European Union has provided 10 years of exclusivity upon drug approval and another two years if the orphan drug works in children.5 This has had an impact. The clinical pipeline for rare and metabolic disease therapeutics has grown by 66% from 2015 to 2019, compared to a mere 3% growth for CVD therapeutics in the same period.2

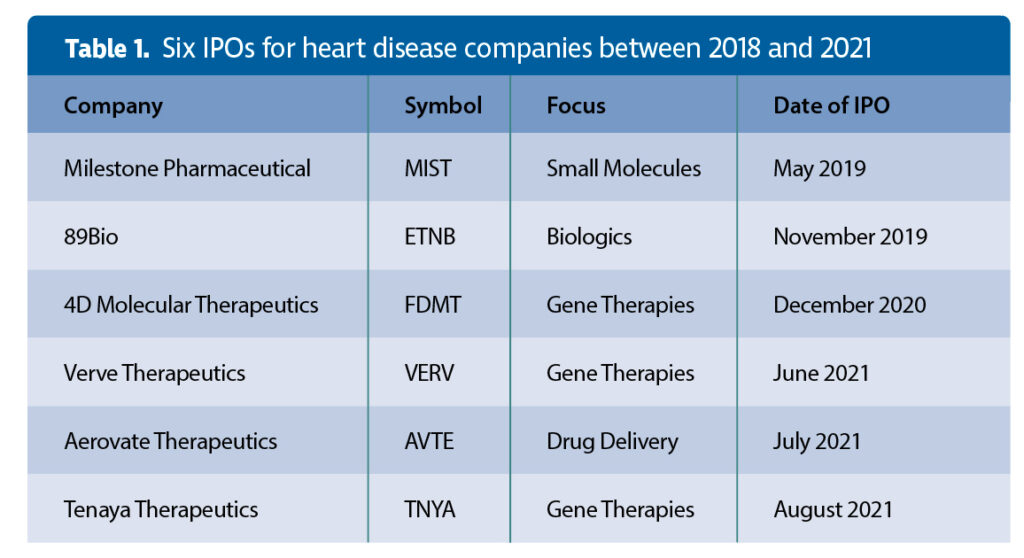

According to a survey of therapeutic biotech initial public offerings (IPOs) of $50 million and higher since 2018,6 there were a total of 100 IPOs for cancer therapeutic companies and 32 for rare disease therapeutic companies from 2018 until August 5, 2021. But by my count, there were only six IPOs for heart disease companies (bundled into the “other” category of the summary tables6). Only one of the six companies is developing a biologic (Table 1).

Applying incentives to CVD therapeutics

Extending market exclusivity to CVD drugs upon approval is a beneficial policy that can remedy the short patent term limits that were conceived by policy makers decades ago. Since 1995, any therapy that receives a patent has 20 years of exclusivity from the earliest date the inventor filed for the patent and not from the date the patent was issued.

Regulatory agencies must consider addressing investor concerns about the size and length of CVD therapeutic clinical trials that narrow the patent protection window by extending market exclusivity after patent protection expires in proportion to the length of the trials being required. By using a formula that factors in the number of subjects or the time it takes to complete the aggregation of clinical trials or both, regulatory agencies will have a vested interest in approving statistically significant but efficient studies that quickly get to the finish line.

We might consider exploring other avenues before tampering with patent treaties. However, we might also consider the view held by many stakeholders in CVD drug development. At two meetings—a European Society of Cardiology (ESC) workshop (in March 2014)7 and a “think tank” meeting in Washington, DC (in July 2014)1—stakeholders in CVD drug development accepted the necessity of large pragmatic trials, but they also suggested that studies should be streamlined and operating costs reduced. That was seven years ago, but the investment landscape has not changed. To be fair, in a seven-page report, the ESC did have one sentence suggesting extended patent protection be considered.7

It takes about 4.5 years to secure a biotechnology patent, and about 10 years to obtain approval from the FDA or its international equivalents by running multiple pivotal clinical trials. CVD therapeutic clinical trials can require thousands of participants to achieve statistical significance, whereas a rare cancer or orphan drug study can have fewer than a hundred. Various forms of CVD are often the consequence of complex genetic and environmental factors in a patient, unlike many cancers whose causes can be isolated to specific gene mutations; hence, progression of a cardiac pathology can require several years of clinical monitoring to determine product efficacy in a properly powered study.

For an example of a “rapid” CVD therapeutic development timeline, see the sidebar, “Appreciating the Size and Length of Clinical Trials for CVD Therapeutics.” Notice that it took Sanofi and Regeneron Pharmaceuticals 12 years from the discovery of PCSK9 as a target for lowering “bad cholesterol” until the biologic Praluent (alirocumab) received FDA approval. That’s fast! An analysis of 113 first-in-class drugs for a variety of clinical indications approved by the FDA from 1999 to 2013 found that it took, on average, 22 years from the first scientific publication describing the therapeutic to the therapeutic’s approval.8

Orphan drug exclusivity begins after drug approval and may extend beyond patent expiration. I propose CVD exclusivity must begin post-patent expiration. But some experts have reservations. They point out that of 217 orphan drugs that are no longer protected either by patents or exclusivity, nearly half still have no generic competitors.9 The markets for orphan drugs are just too small, in contrast to those for CVD therapeutics, which would address some of the world’s most prevalent diseases.

However, experts should also be aware that generic competitors who have avoided the costs of developing a novel cardiac drug need only duplicate a single pivotal clinical trial and show non-inferiority of their biosimilar to reap the benefits once the patent has expired for a CVD therapy. For biotechnology and “big pharma” companies, this increases the risk of not recouping investments in the original innovation.

Bringing biotech to bear in CVD

The advancements in biotechnology that have revolutionized cancer therapies have yet to bring about improvements in CVD therapies. Companies like ours believe a whole host of conditions can be treated with the latest therapeutic innovations; nonetheless, we need the incentives that will draw in greater numbers of investors. Drugs to treat the biggest health threat in much of the world should garner the same attention that orphan drugs do. A successful CVD therapeutic exclusivity program would improve the innovation efforts that are currently lacking.

Missag Hagop Parseghian, PhD ([email protected]), is chief scientific officer and co-owner of Rubicon Biotechnology.

References

1. Fordyce CB, Roe MT, Ahmad T, et al. Cardiovascular Drug Development: Is It Dead or Just Hibernating?

J. Am. Coll. Cardiol. 2015; 65: 1567–1582.

2. Thomas D, Wessel C. The State of Innovation in Highly Prevalent Chronic Diseases. Volume V: Systemic Hypertension and Congestive Heart Failure. BIO Industry Analysis Report (Highly Prevalent Chronic Disease Series). BIO; 2020.

3. Downing NS, Aminawung JA, Shah ND, et al. Clinical Trial Evidence Supporting FDA Approval of Novel Therapeutic Agents, 2005–2012. 2014; JAMA 311: 368–377.

4. Wood S. Glory—Is cancer beating cardiovascular disease? Medscape. Published: August 18, 2021.

5. European Medicines Agency. Rare diseases, orphan medicines: Getting the facts straight. Report No. EMA/551338/2017.

6. Fidler B. A record number of biotechs are going public. Here’s how they’re performing. BioPharma Dive. Accessed: June 26, 2021.

7. Jackson N, Atar D, Borentain M, et al. Improving clinical trials for cardiovascular diseases: a position paper from the Cardiovascular Round Table of the European Society of Cardiology. Eur. Heart J. 2016; 37: 747–754.

8. Eder J, Sedrani R, Wiesmann C. The discovery of first-in-class drugs: origins and evolution. Nat. Rev. Drug Discov. 2014; 13: 577–587.

9. Aitken M, Kleinrock M. Orphan Drugs in the United States: Exclusivity, Pricing and Treated Populations. IQVIA Institute for Human Data Science. December 2018.