May 15, 2016 (Vol. 36, No. 10)

Eric S. S. Langer President and Managing Partner BioPlan Associates

To Know Where Biosimilars Are Going, We Need Better, More Specialized Information Resources

Biosimilars (and related biobetters) represent a new biopharmaceutical product category as well as a new industry segment. So far, over 20 biosimilars have been approved in major markets, primarily the European Union. Only two biosimilars have been approved in the United States.

Most agree that the biosimilars segment will grow quickly and generate many biopharmaceutical products, innovations, and manufacturing facilities. But there is little consensus with regard to basic industry metrics. For example, sales forecasts for the next five years commonly vary by an order of magnitude, from $2 billion to $20+ billion/year. There is not even agreement yet on what names should be used for existing biosimilars.

For the most part, information resources about and supporting biosimilar development have yet to be developed. This is particularly true for data related to bioprocessing and other more technical aspects.

The poor state of biosimilars-related information resources is due to a lack of granularity. For example, few information resources specialize in biopharmaceutical products or related bioprocessing information, much less biosimilars. Where biopharmaceutical and biosimilars information resources do exist, their number, diversity, and sophistication are generally limited. Industry sources, such as trade associations, have not developed biosimilars information resources, and the limited public information the FDA provides generally lacks substance.

Assessing Impacts

Resources that monitor the biosimilars pipeline (what’s in development and marketed) and characterize the industry sgement’s practices include the Biosimilars/Biobetters Pipeline Database. It covers more than 1,350 follow-on biopharmaceuticals worldwide, including >730 biosimilars and >480 biobetters (similar but too different or novel to be approved as a biosimilar), with >600 involved companies.

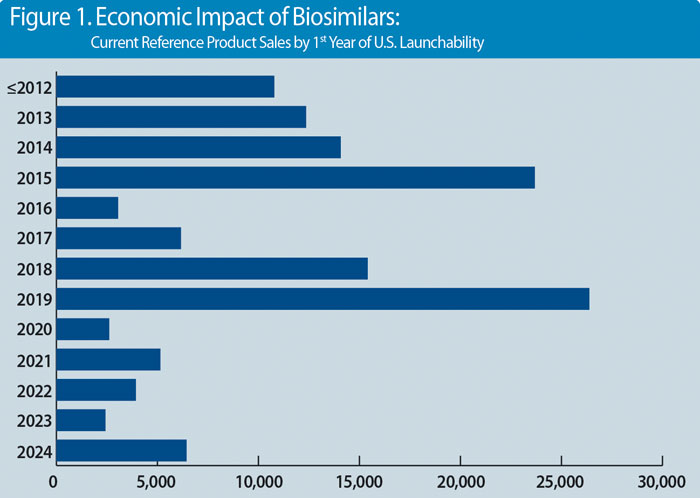

The projected U.S. economic impact of biosimilars (in terms of the current reference product sales by year of their patent/exclusivities expiration) is shown in Figure 1. The data suggests that the United States can expect two waves of biosimilars. One wave appears to have just started. Another is expected at the end of the decade. Both reflect interest in high-revenue, blockbuster products.

Pipeline resources indicate that biosimilars will involve levels of competition among products unprecedented in the biopharmaceutical industry. Also, the evolution of biosimilars is expected to be similar to that of generic drugs.

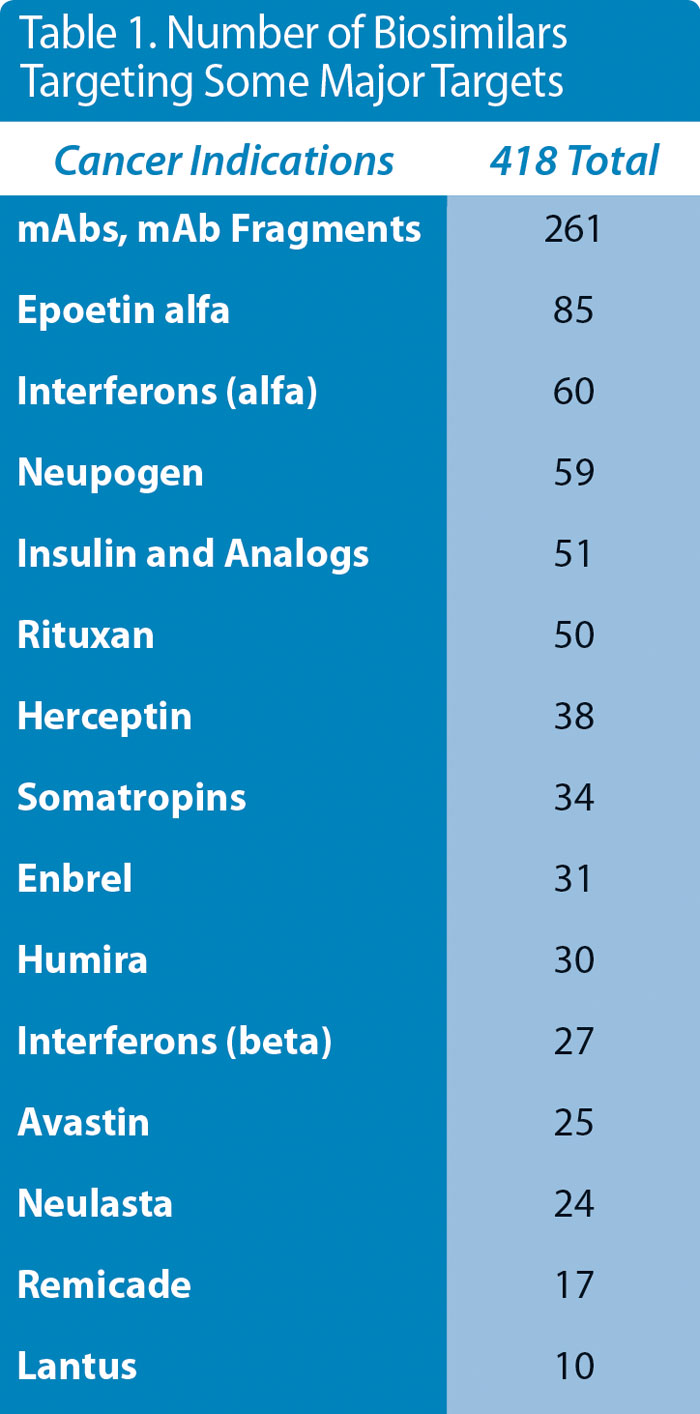

Along these lines, Table 1 shows the high numbers of biosimilars (including biogenerics) in the pipeline targeting some current major products. Based on such data, BioPlan Associates expects an eventual average of eight or more biosimilars entering the U.S. and other major markets for each candidate reference product. (Reference products include >100 marketed recombinant proteins/monoclonal antibodies). Soon enough, biosimilars will considerably outnumber innovative and other reference biopharmaceutical products.

Developing Resources

The first online resource, the Biosimilars/Biobetters Pipeline Database, provides key information on what is in the pipeline. Still in development are resources similar to the Top 1000 Global Biopharmaceutical Index, a free database ranking over 1,000 biopharmaceutical bioprocessing facilities worldwide by reported or estimated capacity. Similar databases are in development for biosimilars manufacturing facilities worldwide. To establish clear strategic manufacturing pathways, the industry requires trend data related to the production of biosimilars, biobetters, as well as lesser-market biogenerics.

Eric S. Langer ([email protected]) is president and managing partner at BioPlan Associates.